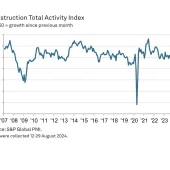

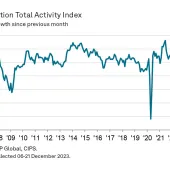

Construction activity rises at fastest pace for 26 months

The UK construction sector has experienced accelerated growth during the second half of the year. During the month of July, there were much faster increases in both activity and new orders. The headline S&P Global UK Construction Purchasing Managers’ Index (PMI) rose sharply to 55.3 in July from 52.2 in June.

This data signalled a marked monthly expansion in total activity in the construction sector, extending the current sequence of growth to five months. Moreover, the rate of expansion was the fastest since May 2022.

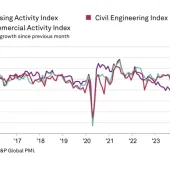

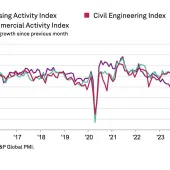

All three categories of construction: Housing; Commercial and Civil Engineering saw activity increase in July as work on housing projects returned to growth. Commercial activity increased solidly, but the fastest expansion was seen in civil engineering activity, where the rate of growth quickened to the sharpest in almost two-and-a-half years.

According to respondents, success in securing new orders was the main factor leading to a rise in construction activity at the start of the third quarter. New business expanded for the sixth month running, and at a marked pace that was the strongest since April 2022. Alongside a general improvement in market demand, there were also reports that customer confidence had strengthened, making them more willing to release previously paused projects.

Construction firms remained strongly optimistic that activity will expand over the coming year, although sentiment dipped to a three-month low in July. Improving client confidence is predicted to help lead to growth of new orders and subsequently activity, with close to 53% of respondents predicting a rise in activity over the next 12 months.

Andrew Harker, economics director at S&P Global Market Intelligence, said: "The election-related slowdown in growth seen in June proved to be temporary, with the pace of expansion roaring ahead in July. Firms saw the strongest increases in new orders and activity since 2022 as paused projects were released amid reports of improved customer confidence.

"The strength of demand moved the sector closer to capacity, bringing a recent period of improving supplier performance to an end. There were also signs of inflationary pressures picking up, something that will need to be watched closely if demand strength continues in the months ahead."

Subscribe to the weekly newsletter